Statutory compliance is crucial in payroll management to uphold responsible business practices. Complying with federal and state employment laws is more than a legal duty; it represents an ethical commitment to employees and protects against significant financial penalties.

However, with regulations spanning federal, state, and even local levels, managing compliance can be overwhelming. This guide cuts through the complexity, offering you a clear, practical path to understanding statutory compliance in the U.S., navigating key legal requirements, and implementing effective compliance practices to keep your business secure and thriving.

Types of Statutory Compliance

Statutory compliance requirements are multifaceted, arising from different government levels and tailored to specific industries. To ensure smooth operations, businesses must navigate federal, state, and industry-specific regulations.

Failure to comply with any of these levels can result in fines, lawsuits, reputational harm, or even shutdowns.

Below is a detailed breakdown of the different types of statutory compliance.

Federal Compliance

The federal government enforces various laws that apply to businesses across the United States, regardless of their location. These laws cover areas such as workplace safety, fair trade practices, environmental protection, taxation, and consumer safety.

Businesses must comply with these regulations to ensure they remain operational, competitive, and legally sound.

Key Federal Agencies and Their Roles

- Occupational Safety and Health Administration (OSHA)

OSHA, an agency under the Department of Labor, is responsible for ensuring employees’ safe and healthy working conditions. It develops safety standards, enforces workplace inspections, and provides training programs to prevent accidents and injuries.- Key Responsibilities:

- Conducting safety inspections to identify and address hazards.

- Enforcing standards for workplace ergonomics, machinery, hazardous materials, and employee health protocols.

- Imposing fines or penalties for non-compliance.

- Impact on Businesses: Companies must ensure that their workplaces meet OSHA standards, provide personal protective equipment (PPE), and maintain proper documentation of safety protocols. Failing to comply can lead to fines, employee lawsuits, and even temporary shutdowns.

- Key Responsibilities:

- Federal Trade Commission (FTC)

The FTC protects consumers by preventing unfair, deceptive, and anti-competitive practices. It ensures that companies operate transparently and promotes healthy market competition.- Key Responsibilities:

- Enforcing antitrust laws to prevent monopolistic behavior.

- Monitoring advertising practices to ensure truthfulness and fairness.

- Regulating consumer data privacy under laws like the Gramm-Leach-Bliley Act (GLBA).

- Impact on Businesses: Companies need to align their advertising practices, pricing strategies, and customer communication with FTC guidelines. Violations can result in hefty fines and damage to brand reputation.

- Key Responsibilities:

- Food and Drug Administration (FDA)

The FDA regulates the safety, quality, and efficacy of food products, pharmaceuticals, medical devices, and cosmetics. This agency ensures that products meet standards to protect public health.- Key Responsibilities:

- Monitoring the manufacturing, labeling, and marketing of drugs and food items.

- Conducting inspections and approving new drugs and devices for public use.

- Enforcing recalls in case of product safety violations.

- Impact on Businesses: Companies in the food and pharmaceutical sectors must adhere to FDA regulations regarding product safety, labeling, and testing. Non-compliance can result in product recalls, lawsuits, and financial penalties.

- Key Responsibilities:

State Compliance

While federal laws provide a baseline, individual states enforce additional regulations that reflect local priorities and needs. These state-level regulations vary widely, meaning businesses operating in multiple states must carefully manage compliance across jurisdictions.

Key Aspects of State Compliance

- Labor Laws

State-specific labor laws cover areas such as wages, overtime, rest breaks, and employee benefits. For example, California enforces stricter wage and hour laws than many other states, including meal and rest breaks requirements.- Impact on Businesses: Companies must stay informed about state-specific employment laws and maintain accurate payroll practices to avoid lawsuits and penalties.

- Tax Obligations

In addition to federal taxes, businesses must comply with state tax laws, which may include income taxes, sales taxes, and property taxes.- Impact on Businesses: Each state has its own tax structure and deadlines, requiring businesses to coordinate closely with tax advisors to meet their obligations. Failure to comply can lead to audits, penalties, and interest charges.

- Environmental Regulations

States like California and New York enforce stringent environmental regulations that may go beyond federal standards. These regulations often cover emissions, waste disposal, and water usage.- Impact on Businesses: Manufacturing companies, in particular, must align their practices with both federal and state environmental laws to avoid penalties and reputational damage.

- Industry-Specific Regulations

States may also have unique requirements tailored to specific industries, such as construction, transportation, and healthcare.- Impact on Businesses: Companies operating in specialized sectors must conduct state-specific compliance assessments and adapt their policies accordingly.

Industry-Specific Compliance

Certain industries face unique regulatory challenges that require tailored compliance efforts. These industries often operate in sensitive sectors where violations can severely affect public health, safety, or financial stability.

Healthcare Industry Compliance

- Health Insurance Portability and Accountability Act (HIPAA)

HIPAA mandates the protection of sensitive patient information and applies to healthcare providers, insurers, and business associates handling medical data.- Key Requirements:

- Implementing secure data storage and encryption to protect patient records.

- Limiting access to health information to authorized personnel only.

- Providing HIPAA training to employees and reporting breaches within a specific timeframe.

- Impact on Businesses: Healthcare providers must have strict data management protocols to ensure patient privacy. Non-compliance can result in steep fines, legal action, and loss of patient trust.

- Key Requirements:

- Food and Drug Regulations (FDA Compliance)

Pharmaceutical companies, hospitals, and clinics must comply with FDA standards for drug approval, medical devices, and treatment protocols.- Impact on Businesses: Failure to meet FDA requirements can result in product recalls and legal liabilities.

Financial Industry Compliance

- Sarbanes-Oxley Act (SOX)

SOX focuses on financial reporting and accountability for publicly traded companies. It aims to prevent fraudulent activities by ensuring the accuracy and transparency of financial statements.- Key Requirements:

- Establishing internal controls and procedures for accurate financial reporting.

- Conducting annual independent audits to verify financial statements.

- Holding executives accountable for certifying the accuracy of reports.

- Impact on Businesses: Publicly traded companies must implement robust financial controls to meet SOX requirements. Non-compliance can result in legal penalties and loss of investor confidence.

- Key Requirements:

- Dodd-Frank Act

Enacted after the 2008 financial crisis, the Dodd-Frank Act regulates banking and financial institutions to promote stability and protect consumers from unfair practices.- Key Requirements:

- Implementing risk management strategies for financial transactions.

- Reporting derivatives and other financial instruments to regulatory bodies.

- Creating consumer protection frameworks, such as clear lending practices.

- Impact on Businesses: Financial institutions must closely monitor compliance to avoid fines and reputational damage.

- Key Requirements:

Manufacturing Industry Compliance

- OSHA Compliance

OSHA standards are crucial for manufacturing companies, where workplace hazards are more common. Businesses must implement safety measures, conduct regular inspections, and ensure workers are trained to handle equipment safely.- Impact on Businesses: Non-compliance with OSHA regulations can lead to severe fines, legal action, and higher insurance premiums.

- Environmental RegulationsManufacturing companies must also comply with state and federal environmental regulations regarding emissions, hazardous waste disposal, and energy consumption.

- Impact on Businesses: Violations can result in fines, operational shutdowns, and reputational harm.

Key Areas of Statutory Compliance

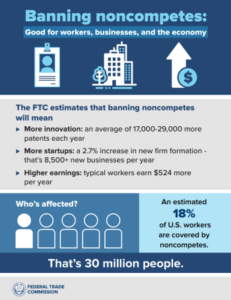

source: Federal trade commission

1. Employment Law Changes

- Overtime Pay Regulations: As of July 1, 2024, the U.S. Department of Labor (DOL) implemented new overtime rules that raised the salary threshold for exempt employees to $55,000 per year. This change is expected to impact nearly 1 million workers initially, with a second increase scheduled for January 1, 2025, potentially affecting an additional 3 million workers.

- Noncompete Clauses: The Federal Trade Commission (FTC) has enacted a rule prohibiting most employers from enforcing noncompete clauses, effective September 4, 2024. This regulation aims to enhance worker mobility and competition in the labor market.

- State-Level Developments: Many states are increasing minimum wage rates, expanding paid sick leave protections, and broadening anti-discrimination laws to include protections based on hairstyle and texture.

2. Data Protection and Privacy Regulations

- New Data Rights Rule: The Consumer Financial Protection Bureau (CFPB) has introduced a sweeping rule to modernise data privacy in banking. This rule mandates that banks and credit card companies comply with new data privacy standards, enhancing consumer rights regarding their personal data.

- AI Regulations: There is growing scrutiny over using artificial intelligence in compliance practices across industries. New guidelines from various regulatory bodies are emerging to address risks associated with AI technologies, particularly in the financial services and insurance sectors.

3. Payroll Compliance Updates

- Tax Changes for 2024: Key payroll compliance updates include an increase in the Social Security wage base to $168,600 and adjustments to health flexible spending arrangement (FSA) contribution limits, which have risen to $3,200. Employers must also be aware of changes in federal income tax rates and withholding requirements.

- Fair Labor Standards Act (FLSA): Compliance with the FLSA remains critical as it governs minimum wage and overtime pay standards across the country. Employers must adhere to federal and state regulations regarding employee classification and compensation.

Key Regulations Impacting Businesses

Health Insurance Portability and Accountability Act (HIPAA)

HIPAA, enacted in 1996, establishes national standards for protecting the privacy and security of sensitive patient health information (PHI). It applies to healthcare providers, health insurers, and business partners handling medical records, including third-party billing companies and IT vendors.

Key Requirements

- Privacy Rule: This rule establishes standards to protect individuals’ medical records and requires businesses to limit the sharing of patient information to authorized entities.

- Security Rule: This rule focuses on the electronic protection of health information, mandating the use of encryption, secure data transmission, and access controls.

- Breach Notification Rule: Requires entities to notify affected individuals, the U.S. Department of Health and Human Services (HHS), and sometimes the media in the event of a data breach involving unsecured PHI.

- Training and Compliance Programs: Healthcare entities must train employees on privacy protocols and conduct regular compliance assessments.

Impact of HIPAA on Businesses

Compliance with HIPAA ensures patient trust and protects businesses from severe penalties, including fines of up to $1.5 million per violation category per year. Non-compliance can lead to reputational damage and the loss of patients’ confidence in healthcare providers.

Sarbanes-Oxley Act (SOX)

The Sarbanes-Oxley Act, enacted in 2002 in response to major corporate scandals (e.g., Enron and WorldCom), aims to protect investors by increasing corporate transparency and improving financial reporting standards for publicly traded companies.

Key Requirements

- Internal Controls: Companies must implement internal controls to ensure accurate financial reporting and detect fraudulent activities.

- Audit Committees: Public companies must establish independent audit committees to oversee financial reporting and work with external auditors.

- CEO and CFO Certification: Top executives must certify the accuracy of financial statements and internal controls, making them personally accountable for any discrepancies.

- Whistleblower Protections: Employees must have a secure channel to report fraud or unethical practices without fear of retaliation.

Impact on Businesses

SOX compliance enhances investor confidence and promotes accountability. However, implementing SOX controls requires significant resource investment, including audits and technology systems. Non-compliance can lead to financial penalties, criminal charges, and a loss of public trust.

Dodd-Frank Wall Street Reform and Consumer Protection Act

The Dodd-Frank Act, passed in 2010 in response to the 2008 financial crisis, introduces comprehensive reforms to reduce systemic risks in the financial industry. The law promotes financial stability, enhances transparency, and protects consumers from predatory practices.

Key Requirements

- Regulation of Financial Institutions: Banks and large financial institutions must maintain higher levels of capital and liquidity to reduce risks.

- Consumer Financial Protection Bureau (CFPB): This bureau was established to oversee and regulate financial products, including mortgages, credit cards, and loans, ensuring consumers are treated fairly.

- Volcker Rule: Limits banks from engaging in speculative investments and proprietary trading, reducing the risk of financial losses.

- Derivatives and Risk Management: Financial institutions must report derivatives transactions and adhere to risk management protocols.

Impact on Businesses

Dodd-Frank has significantly increased compliance costs for financial institutions, as they must allocate more resources to risk management, reporting, and audits. However, the law also fosters a more stable financial environment by curbing risky behavior and protecting consumers.

California Consumer Privacy Act (CCPA)

The CCPA, which came into effect in 2020, grants California residents new privacy rights and imposes strict requirements on businesses that collect, process, or sell personal information.

Even businesses outside of California must comply if they meet specific thresholds related to data processing or revenue generation in the state.

Key Requirements

- Data Transparency: Companies must disclose the categories of personal information they collect, how it is used, and with whom it is shared.

- Consumer Rights: Individuals have the right to access their data, request deletion, and opt out of the sale of their information.

- Notice and Consent: Businesses must provide a “Do Not Sell My Personal Information” link on their websites, allowing consumers to opt out of data sales.

- Security Measures: Companies must implement reasonable security procedures to protect personal data and report breaches promptly.

Impact on Businesses

Non-compliance with the CCPA can result in fines of up to $7,500 per violation, with additional penalties for breaches compromising consumer data. Beyond fines, businesses risk reputational damage and loss of customer trust.

Many companies have had to overhaul their data management processes and invest in privacy technology to comply with the law.

Payment Card Industry Data Security Standard (PCI DSS)

The PCI DSS is not a law but a set of security standards developed by major credit card companies (e.g., Visa, MasterCard, and American Express) to protect cardholder data during transactions. Compliance is mandatory for any business that processes, stores, or transmits credit card information.

Key Requirements

- Secure Network: Businesses must implement firewalls and encryption to protect cardholder data from unauthorized access.

- Access Control: Companies must restrict access to card data to only authorized personnel and regularly monitor access logs.

- Data Encryption: Cardholder data must be encrypted when stored or transmitted across public networks.

- Vulnerability Management: To mitigate potential risks, businesses must conduct regular security scans, vulnerability assessments, and software updates.

- Incident Response: Companies must have a response plan to address data breaches, including notifying customers and credit card companies.

Impact on Businesses

PCI DSS compliance helps businesses prevent data breaches and protect consumer trust. However, compliance can be costly, especially for small businesses, as it requires investment in security systems, training, and regular audits.

Non-compliance can result in fines from credit card companies, increased transaction fees, and the potential loss of the ability to process card payments.

Achieving and maintaining compliance is essential for businesses to avoid legal penalties, build trust, and ensure smooth operations. The process of achieving compliance requires a structured approach, involving assessments, policies, training, and monitoring. Below is a detailed, step-by-step guide to help businesses establish and maintain a robust compliance framework.

Steps to Achieve Compliance

1. Conduct a Compliance Assessment

The first step towards achieving compliance is understanding which laws and regulations apply to your business based on your industry, location, and operational practices.

A compliance assessment helps businesses identify gaps and risks that need to be addressed to meet regulatory requirements.

Key Steps in a Compliance Assessment

- Identify Relevant Laws and Regulations:

- Determine applicable federal, state, and industry-specific regulations.

- Consider laws related to employee rights, data privacy, environmental protection, financial reporting, and consumer protection.

- For example, a healthcare business must comply with HIPAA, while a financial institution must adhere to SOX or Dodd-Frank regulations.

- Engage with Legal Experts:

- Consulting with legal experts or compliance consultants helps businesses interpret complex regulations accurately.

- Experts can also provide insights into best practices, industry trends, and any upcoming regulatory changes.

- Conduct Internal Audits:

- Review existing policies, processes, and documentation to assess your current compliance status.

- Identify gaps between current practices and legal requirements, and document areas for improvement.

- Create a Risk Mitigation Plan:

- Prioritize areas of non-compliance based on the potential impact and develop a roadmap to address these risks.

- For example, if a company stores sensitive customer data but lacks encryption, implementing security measures should be a top priority.

Outcome:

A thorough compliance assessment clearly understands your legal obligations and highlights gaps that need immediate action. This step ensures you start with a solid foundation for further compliance efforts.

2. Develop a Compliance Policy

A well-defined compliance policy serves as a blueprint for meeting regulatory requirements. It communicates the company’s commitment to compliance and provides employees with guidance on adhering to laws and internal rules.

Key Components of a Compliance Policy

- Define Objectives and Scope:

- Specify the policy’s purpose, such as protecting customer data, ensuring workplace safety, or adhering to financial regulations.

- Clearly outline which laws and standards the policy covers and which departments or employees it applies to.

- Outline Procedures and Guidelines:

- Provide step-by-step instructions on how the company will meet each regulatory requirement.

- For example, for data privacy compliance (e.g., CCPA), include procedures for responding to customer data requests or breach notifications.

- Assign Roles and Responsibilities:

- Designate specific individuals or teams responsible for monitoring compliance activities.

- Appoint a compliance officer or a compliance committee to oversee the implementation and enforcement of policies.

- Document Reporting and Communication Processes:

- Include procedures for internally reporting non-compliance or suspicious activities.

- Ensure that there are communication channels for employees to raise concerns without fear of retaliation (aligned with whistleblower protections).

- Update Policy Regularly:

- Regulations and business operations evolve over time. The policy should have built-in mechanisms for updates and revisions.

Outcome:

A comprehensive compliance policy ensures that everyone within the organization understands their role in maintaining compliance. It fosters a culture of accountability and makes enforcing standards across the company easier.

3. Implement Training Programs

Training is a crucial component of compliance because it ensures that employees understand their responsibilities and are equipped to meet regulatory requirements. Regular, well-designed training programs minimize risks by fostering awareness across the organization.

Key Aspects of Compliance Training

- Identify Key Training Areas:

- Focus on the regulations most relevant to your business. For example:

- Healthcare providers must train employees on HIPAA regulations.

- Financial institutions should focus on compliance with anti-money laundering (AML) and SOX regulations.

- Focus on the regulations most relevant to your business. For example:

- Develop Customized Training Modules:

- Tailor training content to specific roles and departments. Employees handling sensitive data may require more in-depth data security training than other staff members.

- Use a mix of formats, such as in-person workshops, online courses, and interactive quizzes, to increase engagement.

- Ensure Continuous Training:

- Compliance requirements change over time. Regular refresher courses keep employees updated on new regulations or internal policy changes.

- For example, with data privacy laws like the CCPA and GDPR constantly evolving, annual updates are essential.

- Track and Document Training:

- Maintain records of all training sessions, including attendance logs and completion certificates.

- Tracking training helps ensure compliance during audits and demonstrates the company’s commitment to employee education.

Outcome:

Effective training programs reduce the likelihood of non-compliance incidents by ensuring that employees are well-prepared to meet legal requirements. Regular training also reinforces a culture of compliance throughout the organization.

4. Establish Monitoring Mechanisms

Achieving compliance is not a one-time task—it requires continuous monitoring and oversight. Ongoing audits, assessments, and reporting systems help businesses stay compliant and proactively address potential issues before they escalate.

Key Elements of Compliance Monitoring

- Set Up Internal Audits:

- Regularly review business processes, financial transactions, and documentation to ensure ongoing compliance.

- Schedule audits based on the criticality of operations—for example, conduct monthly reviews for financial processes and quarterly assessments for workplace safety.

- Implement Compliance Software:

- Use compliance management software to automate monitoring, generate reports, and track key metrics.

- For example, financial institutions may use software tools to monitor transactions for suspicious activities as part of their AML compliance efforts.

- Establish Reporting Channels:

- Create mechanisms for employees to report potential compliance breaches or unethical behavior confidentially.

- Whistleblower policies, required under SOX, help identify issues early and prevent larger problems.

- Monitor External Changes:

- Stay informed about changes in relevant laws, such as updates to the PCI DSS, new state tax laws, or amendments to labor regulations.

- Subscribing to legal bulletins or using regulatory tracking tools helps ensure your business is always aligned with the latest requirements.

- Develop Incident Response Plans:

- Have a plan in place to respond quickly to compliance breaches or data breaches.

- For example, in the event of a cybersecurity breach involving credit card data, businesses must follow PCI DSS protocols to notify affected parties and credit card companies.

Outcome:

Establishing monitoring mechanisms ensures that compliance efforts remain effective over time. Regular audits and reporting systems allow businesses to detect and address potential risks early, minimizing the impact of non-compliance incidents.

Maintaining Compliance

Maintaining compliance is an ongoing process that requires continuous monitoring, documentation, and regular policy updates. It ensures that businesses remain aligned with evolving regulations and internal standards, reducing non-compliance risk.

1. Documentation Requirements

Accurate and comprehensive documentation is the backbone of a strong compliance program. Proper record-keeping proves that your business is adhering to relevant laws and regulations.

These records demonstrate compliance efforts during audits or inspections and help organizations avoid fines, penalties, or legal issues.

Types of Documentation to Maintain

- Meeting Minutes

- Record decisions made during board meetings, management meetings, or compliance committee discussions.

- Meeting minutes provide a clear trail of how compliance issues are addressed, including policy changes or corrective actions.

- Employee Records

- Keep records of employee contracts, background checks, payroll, training sessions, and disciplinary actions.

- Employee documentation helps businesses comply with labor laws, such as the Fair Labor Standards Act (FLSA) and anti-discrimination regulations.

- Financial Statements and Reports

- Maintain accurate financial records, including income statements, balance sheets, tax filings, and audit reports.

- For publicly traded companies, financial documentation is critical for meeting Sarbanes-Oxley Act (SOX) requirements and providing transparency to investors.

- Audit Results and Compliance Reports

- Document internal and external audit findings, as well as any corrective actions taken.

- Maintaining these records ensures accountability and helps identify recurring issues that may need further attention.

- Policies and Procedures Manuals

- Store updated copies of compliance policies, employee handbooks, and operational procedures.

- These documents help businesses train employees and serve as a reference during audits or regulatory reviews.

- Incident Reports

- Document any incidents related to non-compliance, data breaches, or workplace safety violations, along with the actions taken to resolve them.

- This ensures transparency and accountability, demonstrating that the business has mechanisms to promptly address issues.

Importance of Proper Documentation

- Evidence of Compliance: Regulative bodies often require proper documentation during audits or investigations to confirm adherence to laws.

- Risk Mitigation: Detailed records help businesses track trends and identify potential risks before they escalate.

- Operational Continuity: Accurate documentation ensures that compliance processes can continue smoothly even if key personnel leave or transfer roles.

- Avoiding Legal Liability: In the event of a dispute, documentation serves as proof that the business acted responsibly and in accordance with the law.

2. Regular Updates and Reviews

Laws and regulations are subject to frequent changes, driven by new industry standards, government policies, and technological advancements. Regular updates and reviews of compliance policies and procedures are essential to ensure that businesses remain aligned with current legal requirements.

Why Regular Updates are Necessary

- Evolving Regulatory Landscape

- New laws, amendments to existing laws, and changes in industry standards can impact business operations. For example, updates to data privacy laws such as the California Consumer Privacy Act (CCPA) may require changes to data management practices.

- Businesses must stay informed about federal, state, and industry regulatory changes to avoid penalties and disruptions.

- Changes in Business Operations

- Expanding into new markets, launching new products, or adopting new technologies can introduce new compliance risks.

- For example, a business that begins handling credit card transactions must comply with PCI DSS security standards, even if it was not previously subject to these requirements.

- Audits and Compliance Gaps

- Regular audits may reveal weaknesses in existing compliance practices. Addressing these gaps promptly requires policy updates and process improvements.

- Continuous monitoring ensures that businesses remain proactive rather than reactive in addressing compliance challenges.

How to Conduct Effective Reviews

- Schedule Periodic Reviews

- Establish a schedule for reviewing compliance policies, such as annually or semi-annually.

- More frequent reviews may be necessary in fast-changing industries, such as finance or healthcare, to keep pace with new regulations.

- Engage Stakeholders

- Include input from legal teams, compliance officers, department heads, and external consultants to ensure that policies reflect the latest regulatory changes.

- Engaging employees in the review process also promotes awareness and encourages accountability at all levels of the organization.

- Use Regulatory Tracking Tools

- Utilize automated tools and software that track changes in relevant laws and send alerts when updates occur.

- These tools help businesses stay ahead of new requirements and avoid missing deadlines for compliance actions.

- Test and Validate Compliance Procedures

- Conduct tests to ensure that compliance procedures are working as intended. For example, run mock audits to evaluate readiness for official inspections.

- Validation helps identify weaknesses and ensures that corrective actions are taken promptly.

- Document Changes and Communicate Them

- Keep records of policy changes and communicate them to all employees and stakeholders.

- Ensure that employees understand how the changes affect their roles and provide any necessary training.

Outcome of Regular Updates and Reviews

- Proactive Compliance Management: Businesses can anticipate and adapt to regulatory changes, reducing non-compliance risk.

- Improved Efficiency: Regular updates ensure that compliance processes remain relevant and efficient, minimizing the need for last-minute fixes.

- Enhanced Reputation: Companies that demonstrate continuous compliance efforts build trust with customers, regulators, and investors.

- Lower Risk of Fines and Penalties: Timely updates help businesses avoid costly fines for non-compliance with newly implemented laws.

Consequences of Non-Compliance

Non-compliance with statutory requirements exposes businesses to a range of serious risks, including legal penalties, financial losses, reputational harm, and even operational shutdowns. Regulations exist to ensure fair practices, consumer protection, workplace safety, and data security.

When businesses fail to adhere to these requirements, the repercussions can be severe, affecting both short-term operations and long-term sustainability.

1. Legal Penalties and Financial Sanctions

The most immediate consequence of non-compliance is exposure to legal action, fines, and sanctions imposed by regulatory authorities. Legal penalties vary based on the type of violation, the severity of the breach, and the laws governing the industry or region.

Types of Legal Penalties

- Fines and Monetary Penalties

- Regulatory bodies impose fines for non-compliance, which can escalate based on the duration and severity of the violation.

- Example: Under the General Data Protection Regulation (GDPR), fines for severe data breaches can reach up to 4% of a company’s global annual revenue or €20 million, whichever is higher.

- Sanctions and Restrictions

- In some cases, regulatory authorities may impose sanctions, such as operational restrictions or limits on market activities, to compel compliance.

- Example: Financial institutions failing to comply with the Dodd-Frank Act may be restricted from making certain types of investments or engaging in certain lending practices.

- Civil Lawsuits

- Non-compliance can lead to consumer, employee, or shareholder lawsuits, resulting in significant legal expenses and compensation payouts.

- Example: A company that violates workplace safety regulations under OSHA may face litigation from injured employees seeking damages.

- Criminal Prosecution

- In extreme cases, deliberate or reckless non-compliance can result in criminal charges against executives or business owners.

- Example: Companies involved in fraudulent financial reporting under SOX may face criminal investigations, and CEOs or CFOs may be subject to imprisonment.

Impact on Businesses

- Legal penalties can severely affect a business’s cash flow and profitability.

- Repeated non-compliance can result in escalating fines, leading to significant financial strain.

- Companies may also incur additional costs related to legal fees, compliance consultants, and audits to address violations.

2. Reputational Damage and Loss of Customer Trust

In today’s highly connected world, non-compliance incidents can quickly become public knowledge through media coverage, social platforms, or customer reviews. This exposure can significantly damage a company’s reputation, eroding customer trust and loyalty.

Consequences of Reputational Damage

- Loss of Customer Base

- Customers are more likely to switch to competitors if they perceive a business as unethical or non-compliant.

- Example: Data breaches that expose personal information often lead to customer churn, as affected individuals lose confidence in the company’s ability to protect their data.

- Negative Publicity

- Non-compliance incidents attract media attention, which can tarnish a company’s brand image. In severe cases, the business may face boycotts or negative campaigns.

- Example: Pharmaceutical companies found guilty of FDA violations have faced public backlash and scrutiny, affecting their market performance.

- Difficulty Attracting Investors and Partners

- A damaged reputation can make it difficult to attract new investors, partners, or clients, as stakeholders prefer to engage with compliant and transparent businesses.

- Example: Publicly traded companies found in violation of SOX regulations may see their stock prices plummet, reducing shareholder value and investor interest.

- Loss of Employee Morale and Talent

- Employees who perceive their company as unethical or poorly managed may feel demotivated or disengaged, and talented professionals may seek employment elsewhere.

- Example: Non-compliance with labor laws or poor workplace safety practices can result in higher employee turnover and recruitment challenges.

Impact on Businesses

- Rebuilding a damaged reputation can take years and require significant investments in marketing, public relations, and community engagement initiatives.

- Companies may need to offer incentives or discounts to regain customer trust, further impacting profitability.

3. Loss of Licenses or Permits

In some industries, regulatory authorities require businesses to obtain licenses, permits, or certifications to operate legally. Non-compliance with relevant laws can result in the revocation or suspension of these licenses, disrupting operations and causing long-term harm.

Examples of License and Permit Revocation

- Healthcare Sector

- Medical facilities found in violation of HIPAA or safety regulations may lose their operating licenses, preventing them from treating patients.

- Example: A hospital with repeated HIPAA violations could face suspension of its Medicare provider license, leading to financial distress.

- Financial Institutions

- Banks and financial firms must comply with anti-money laundering (AML) regulations and financial reporting laws. Non-compliance can result in license revocation.

- Example: The Federal Reserve or other regulatory bodies may revoke the banking license of a bank involved in fraudulent activities.

- Food and Beverage Industry

- Restaurants, food manufacturers, and distributors must comply with FDA regulations regarding food safety. Non-compliance can result in permit suspension or forced closures.

- Example: A restaurant that repeatedly violates health code may have its food service permit revoked, resulting in business closure.

- Environmental Violations

- Manufacturing companies must comply with environmental regulations related to emissions, waste disposal, and water usage. Non-compliance can lead to operational shutdowns or denied permit renewals.

- Example: A factory emitting pollutants beyond permissible limits may have its environmental permit revoked, forcing it to cease operations.

Impact on Businesses

- Losing licenses or permits directly affects a company’s ability to operate, leading to revenue loss, employee layoffs, and customer attrition.

- In industries where licenses are essential, such as healthcare or finance, the loss of operational permits can permanently damage the business’s market position.

- Companies may face significant costs to reinstate licenses, including legal fees, compliance audits, and re-certifications.

Resources for Businesses

Navigating statutory compliance requires access to reliable resources and tools. Businesses can leverage government agencies, professional organizations, and advanced online tools to remain compliant and mitigate risks.

These resources provide guidance, automate processes, and ensure companies stay aligned with changing regulations. Below is an overview of key resources available to businesses.

1. Government Resources

Government agencies provide valuable information on regulations, compliance programs, and best practices. These public resources include templates, guides, and training programs that assist businesses in adhering to laws at the federal, state, and local levels.

Key Government Resources for Businesses

- Small Business Administration (SBA):

- Offers detailed guides on federal laws, labor standards, tax regulations, and industry requirements.

- Provides access to training, funding programs, and webinars for small businesses.

- Occupational Safety and Health Administration (OSHA):

- Develops workplace safety standards, self-assessment tools, and training resources.

- Provides free consultation services to identify potential workplace hazards and prevent accidents.

- Internal Revenue Service (IRS):

- Offers tools for understanding tax laws, calculating employer obligations, and filing taxes.

- Provides e-filing systems and guidance on record-keeping for tax compliance.

- Consumer Financial Protection Bureau (CFPB):

- Regulates financial practices and protects consumers from predatory practices.

- Provides templates, alerts, and best practices for businesses offering financial services.

2. Professional Organizations and Industry Associations

Industry-specific organizations help businesses interpret complex regulations by providing tailored guidance and resources. They offer best practices, certifications, and compliance support to address sector-specific challenges.

Examples of Professional Organizations Supporting Compliance

- American Hospital Association (AHA):

- Supports healthcare providers in complying with HIPAA, CMS guidelines, and other healthcare regulations.

- Offers training, webinars, and publications focused on healthcare compliance.

- Financial Industry Regulatory Authority (FINRA):

- Oversees financial institutions and brokers, providing tools and guidelines for compliance with federal and state standards.

- Offers certification programs and compliance alerts to help firms meet evolving regulations.

- National Restaurant Association (NRA):

- Guides food safety laws, employee training, and labor regulations in the food service industry.

- Offers templates and tools for conducting internal audits and ensuring compliance with FDA rules.

- Society for Human Resource Management (SHRM):

- Provides resources to maintain compliance with labor laws and employee benefit regulations.

- Offers compliance checklists and training modules for HR professionals.

3. Online Tools and Software Solutions

In today’s digital landscape, businesses rely on advanced tools to automate compliance tasks, monitor regulatory changes, and manage documentation. Online solutions help businesses streamline compliance processes, reduce human error, and respond quickly to legal requirements.

Key Online Tools and Software Solutions

- Regulatory Change Tracking Tools

- ComplySci and Regology provide real-time alerts for new or updated regulations.

- These tools help businesses stay ahead of legal changes by notifying them of compliance requirements as they arise.

- Compliance Management Software

- NAVEX Global and LogicGate offer end-to-end solutions to manage risk assessments, compliance audits, and incident reporting.

- These platforms provide dashboards that allow businesses to track their compliance status and address gaps proactively.

- Data Privacy Tools

- OneTrust and TrustArc automate data privacy management to comply with laws such as CCPA and GDPR.

- They manage consent tracking, data subject requests, and privacy impact assessments for businesses.

- Document Management Systems (DMS)

- Tools such as SharePoint and DocuWare enable secure document storage, version control, and easy retrieval during audits.

- Businesses use these systems to maintain organized compliance records and audit trails.

- Learning Management Systems (LMS)

- Litmos and Cornerstone provide compliance training modules to educate employees about regulations and internal policies.

- These systems track employee progress, ensuring that everyone completes mandatory compliance courses on time.

- Juntrax (https://juntrax.com)

- Juntrax is an all-in-one business management platform that ensures compliance with various regulations.

- It provides tools to streamline compliance processes, manage employee documentation, and automate internal audits, ensuring that clients remain free from legal issues.

- Key Benefit: Businesses using Juntrax can centralize their compliance activities, reducing manual effort and ensuring operational transparency.

Benefits of Online Tools and Software Solutions

- Automation: Automates compliance processes, reducing manual errors and saving time.

- Regulatory Alerts: Keeps businesses informed of regulatory changes in real-time.

- Documentation: Centralizes compliance-related documentation for easy access during audits or inspections.

- Training Management: Tracks employee compliance training and ensures department policies are followed.

Emerging Trends in Compliance

- Increased Regulatory Oversight: Federal agencies are passing major regulations affecting various sectors, including healthcare and finance. Compliance practitioners are advised to stay informed about these changes to mitigate risks associated with non-compliance.

- Focus on Consumer Protection: There is a heightened emphasis on consumer protection laws, particularly concerning financial services and data privacy. Organizations must adapt their compliance strategies to align with these evolving standards.

- AI Governance: As AI technologies become more prevalent in business operations, regulatory frameworks are being developed to ensure ethical use and mitigate risks associated with bias and discrimination in automated decision-making processes.